Iran war and the looming prospect of stagflation

Background:

- During the 1970s and early 1980s, most Western countries experienced “stagflation”— a condition where low, if not negative, economic growth coexisted with high inflation.

- During these episodes of stagflation the driver was oil shocks.

- The first one came after the Yom Kippur War between Israel and Egypt-Syria. The Organization of Arab Petroleum Exporting Countries implemented a total oil embargo against the Western nations that had supported Israel. The second oil crisis happened with Iran’s Islamic Revolution in 1979, followed by Iraq’s invasion of Iran a year later.

- Since that time, the world has witnessed at least three oil shocks — in 2008, 2022 and 2026. The 2008 shock resulted in stagnation (negative to very low single-digit GDP growth), but no runaway inflation. The 2022 Russia-Ukraine war produced some inflation, but no great recession.

Will 2026 see the return of stagflation?

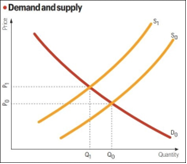

- In standard textbook economics, there is a supply and a demand curve. The supply curve slopes upward from left to right, depicting a positive relationship: as prices rise, producers are encouraged to increase the quantity supplied of a particular good.

- The demand curve, conversely, is downward sloping: Consumers buy more of a good at lower prices and less at higher rates.

Fig: The point where demand and supply curves intersect is the market-clearing equilibrium.

- The accompanying chart shows an initial supply curve (S0) and the demand curve (D0). The point where they intersect is the market-clearing equilibrium. At the equilibrium price P0, the quantity demanded by consumers Q0 matches what the producers offer to supply.

- Stagflation typically arises from “negative supply shocks”. Normally, any increase or decrease in the supply of a good is due to changes in its price, with other factors such as input costs, production conditions and technology remaining the same. The movement here is from one point to another on the same supply curve.

- In a supply shock, the entire supply curve shifts rightward or leftward. Producers would now offer to supply more or less of a good at the same price.

- A positive supply shock is usually thanks to any new productivity-boosting technology (say, AI) or lower input costs, whether of energy or raw materials. The triggers for negative supply shocks are the opposite — from pandemics and natural disasters to wars and closure of vital shipping lanes (think the Strait of Hormuz). The resultant disruptions to production and trade shifts the supply curve to the left.

- One can see the effect of the supply curve shifting from S0 to S1 in the chart. At the new intersection point of the supply curve S1 and D0, not only is the equilibrium price higher at P1, the quantity supplied, too, is lower at Q1. That, in short, is stagflation.

Can that be a real possibility today?

- It depends on the magnitude and duration of the supply shock.

- The present crisis is both a price and a supply shock, making it more pernicious than 2022 or 2008. It isn’t just prices, but the availability of energy itself that has become a question mark.

- When gas or LPG is not available, you risk a sudden stoppage in industrial activity. These sudden stops generate non-linear outcomes in the economy.

- In the 1970s, Indian farmers were only beginning to use chemical fertilisers, while households overwhelmingly relied on firewood and dung cakes for cooking and a miniscule minority wore polyester and nylon fabrics.

- That’s not the case today, where urea and di-ammonium phosphate have practically replaced farmyard manure, LPG cylinder coverage is near-universal, and man-made fibres are ubiquitous.

- Not for nothing the Indian economy is much more vulnerable to what is now a full-fledged energy crisis, impacting not only prices but actual availability of oil, gas and the petrochemical feedstocks and intermediates derived from them that go into a host of downstream industries.

How does one deal with stagflation?

- If the Iran war were to end soon — and assuming that the attacks on the West Asian oil refineries and natural gas processing facilities haven’t caused significant damage from a production restoration standpoint — the supply curve may revert from S1 to S0 quickly.

- Recessions or low single-digit growth rates (like what India has faced in the past) can be addressed through expansionary fiscal and monetary policies.

- Inflation alone can similarly be dealt with by tightening money supply and raising interest rates.

- Neither of these tools works easily in stagflations. Jacking up interest rates to fix one component (inflation) may worsen the other (stagnant growth and high unemployment). Fiscal and monetary loosening to stimulate demand, when supply is constrained, will simply further fuel inflation.

- Given that traditional fiscal and monetary tools are designed to manage demand, they are seen to be ineffective against stagflation, which is primarily a supply-side phenomenon.

- The solutions, then, would lie in repairing and restoring broken supply chains. But that’s easier said than done.